TPG Angelo Gordon secures £100m financing for outdoor storage platform

Leumi UK agrees deal to support TPG and Blomfield Partners’ Concreit

What – TPG Angelo Gordon and operating partner Blomfield Partners have secured a £100m finance package from Leumi UK to support their UK IOS platform

Why – The investors want to develop Concreit in the nascent UK IOS sector

What next – TPG Angelo Gordon is further expanding its IOS investments across Continental Europe

TPG Angelo Gordon and operating partner Blomfield Partners have agreed a finance package of up to £100m with a specialist lender for Concreit, their UK industrial outdoor storage (IOS) platform, Green Street News can reveal.

Leumi UK has agreed terms with the partnership as it looks to develop Concreit, which reached 35 sites before disposing of 12 of them in the past six months as part of ongoing asset management and a capital recycling strategy.

The financing comes at a time when IOS is further developing as a niche real estate strategy in the UK and Europe, following in the footsteps of the more mature US market.

TPG Angelo Gordon has already expanded its IOS investment into Continental Europe. In the Netherlands, the firm has a €200m partnership with DCM Investment Group and has acquired four IOS sites to date, while it has also bought its first site in Germany. The firm confirmed it is also targeting additional European markets with attractive IOS fundamentals.

Supply-demand imbalance

TPG Angelo Gordon said its IOS strategy was underpinned by an “acute supply-demand imbalance”, particularly in core logistics and intermodal transport markets with limited capex requirements and attractive income characteristics.

The firm has an established IOS real estate background in the US through its partnership with Triten Real Estate Partners.

John Parsons, London-based real estate investment professional and principal at TPG Angelo Gordon, said of the financing with Leumi UK: “This transaction marks a significant step in scaling our platform and reflects growing institutional conviction around the IOS opportunity.”

BBS Capital acted as sole adviser on the transaction. Blomfield Partners was founded by Matthew Quicksilver and Alex Telford, and acts as operating partner for the UK strategy.

Last month Leumi UK provided its largest healthcare financing to date, as revealed by Green Street News. The real estate lender provided a £100m revolving credit facility to LNT Care Developments, the UK’s largest care home developer, to support the continued expansion of its care home portfolio.

Market pulse: Alternative lenders vie for business amid bank resurgence

BBS Capital’s Adam Buchler describes today’s debt market as ‘probably the most competitive I’ve seen in almost 20 years’.

Bank lenders are demonstrating strong appetites for financing European commercial real estate, forcing alternative debt providers to think creatively about their plans to deploy capital this year.

A return in strength by banks was noted by multiple debt market participants throughout 2025. Sources explained many banks had focused on enhancing existing clients in recent years but were keen to replenish their loan books as underlying property market conditions improved.

At the same time, alternative lenders have gathered dry powder. Data from affiliate title PERE shows private real estate credit managers raised $54.2 billion globally last year, up from $52.7 billion in 2024.

Speaking to Real Estate Capital Europe in the early part of 2026, debt market sources acknowledge competitive conditions as alternative lenders look for transactions against the backdrop of a resurgent banking sector.

Andrew Gordon, head of real estate debt for Europe at US manager Invesco, describes the return in force of banks as a “double-edged sword” for alternative lenders. “On the one hand, we have definitely seen deals that have gone away from us because the borrower likes our terms at 70 percent loan-to-value, but a bank’s terms at 50 percent are much cheaper, so they opt to go for the lower leverage.

“On the other hand, banks are heavily into providing back leverage. As bank competition drives down back leverage pricing, whole loan pricing subsequently comes down in the cases where Invesco uses it,” he adds.

Richard Craddock, head of real estate debt at Dutch manager Redevco, agrees the return of banks to the sector was the driving factor in a significant increase in liquidity in 2025.

“On the supply side, there was a lot of liquidity, but on the demand side was still constrained by a dysfunctional market, with bid-ask spreads wide. We’ve started this year with liquidity still there on the supply side, but on the demand side we are already seeing an uptick in traditional transactions between willing buyers and sellers, the bid-ask spread has tightened.

“There’s more and lower cost capital on the equity side and that is helping transaction volumes. It’s still early days, but I hope the supply/demand will come into equilibrium and pricing will stabilise.”

Adam Buchler, managing director at London-based debt advisory firm BBS Capital, describes today as “probably the most competitive debt market I’ve seen in almost 20 years”.

It is a challenging time to be a lender, he says. “Every process we run is very well bid and highly competitive, and we often find there’s an outlier with a particular appetite to deploy and so pushes beyond where we sized the original underwriting to pricing right down beyond what we expected. Sometimes, we’ll get improved sets of terms from lenders previously discarded from the process looking to get a position.”

Speaking about the UK market, Buchler says margins can now be as low as early 100 basis points for income-producing, stabilised assets. Development finance, for the best projects and sponsors, can be priced with margins inside 300bps. He adds: “Over the past 12-18 months, for the best projects, margins have probably tightened by 30-50bps.”

Points of difference

On LTV, sources say banks typically offer investment loans in the mid to high-50 percent range. Gordon says LTV varies according to jurisdiction: Spanish and Italian banks are offering lower leverage than their German counterparts.

“Leverage is the main thing that keeps the banks from where we are operating,” he adds. “But there are other points of difference.” In some jurisdictions, the banks are wedded to the major cities. Some banks are still less fond of alternative sectors, and when it comes to construction loans, that gap in LTV between banks and non-banks can be bigger than it is for investment deals.”

There are other ways Invesco wins deals, he says. “First is presence in local markets where you need to be on the ground. Second is competing in jurisdictions that are more complicated in terms of structuring loans, such as Italy or France. And third is the relationship aspect. You can’t get away from the fact that pricing is important, but increasingly, with experienced borrowers, the relationship provides certainty of execution.”

While refinancing still accounts for most activity, sources say acquisition financings are increasing. Those with a transitional aspect to them are creating opportunities for non-bank lenders, some argue.

“With our focus on the lending side on deep refurbishment and development financing, we’re seeing a lot of transitional financing opportunities coming through,” explains Craddock.

“We think it’s the least well served part of the lending market from a supply perspective, so it creates an opportunity for private credit lenders to grow market share on attractive risk-adjusted returns. The banks are still pretty wary – there’s capital there, but such deals require a lot of monitoring, and they just don’t have the internal capabilities to step in and manage out challenged situations.”

Craddock adds transitional lending generates high single-digit returns in today’s market, with the potential to earn double digits with the addition of higher leverage.

By geography, sources say some alternative lenders are exploring the region. Francesca Galante, co-founder of real estate debt adviser First Growth Real Estate & Finance, says: “I find a lot of lender interest in continental Europe. It is targeted towards markets such as Spain, Italy, Greece, Cyprus, markets that were considered more peripheral previously.”

Some asset classes are moving back into favour with lenders, she adds. “Retail is definitely back. Footfall is back to pre-covid levels and assets have repriced, so there is a lot of interest from debt funds and banks. Student housing is still flavour of the month, including prime but also more secondary locations. And we see lender appetite is back for well-priced offices. That applies to banks and non-banks.”

Maintaining discipline

Despite the competitive conditions, sources emphasise the need for alternative lenders to maintain discipline around lending terms and loan covenants. Sources say most alternative lenders are not compromising in such areas to win business.

“There have always been certain borrowers that get covenant-lite deals. Is that number growing? Not a lot. Across all the borrowers in the market, covenant-lite is still an unusual feature,” says Gordon.

“I don’t think this lending cycle has been about migration of risk,” agrees Craddock. “It’s been more about pricing. By and large, the discipline has been there across the market.”

With banks and alternative lenders poised to write loans, competitive lending conditions across European real estate markets are set to persist.

City’s first co-living scheme secures £78m debt as funding hunt begins for second

Bridges and Hub progress funding for Square Mile developments

What: Bridges and Hub have appointed agents to seek a funding partner for 150 Minories scheme, and secured £78.1m loan for 45 Beech Street development

Why: Assemblies and Cornerstone in the City of London have planning for 277 and 174 co-living units respectively

What next: Construction is due to start on Cornerstone following Gateway 2 approval, with completion expected in 2028

Bridges Fund Management and Hub have appointed agents to help them find funding for a co-living scheme in the City of London and secured development finance for another, Green Street News can reveal.

The two schemes, which will be the first co-living developments in the City, have a previously disclosed combined gross development value of £255m.

Savills is understood to have been appointed to explore funding options for the Assemblies scheme at 150 Minories, a 277-home development that received planning in April 2025. The pair bought the site in November 2023 for £39m from BE Offices as part of their growing office-to-residential development pipeline.

It will be the second co-living development in the City, with the first – Cornerstone, at 45 Beech Street – also being developed by Hub and Bridges.

Rather than find an equity partner, the pair are bringing the Beech Street scheme forward themselves, and have secured a £78.1m development loan from Firma Partners. Bridges has significant investment firepower, having just raised £440m for its Bridges Property Alternatives Fund VI.

Located at the edge of the Barbican Estate, the Beech Street scheme will convert and extend a 1950s office building into 174 co-living homes. Hub and Bridges bought the office in 2023 for £30m, before receiving planning in 2024.

Simon Ringer, head of Bridges Property Funds, said: “Our funds have now secured positions in a platform of co-living schemes in prime locations in London, and we look forward to building these out for operation in a market that is starved of high-quality, flexible residential accommodation.”

The two schemes form part of the City’s shift to bring forward more residential in the Square Mile through its Destination City strategy, which allows limited residential development in certain areas to increase out-of-hours footfall, notably for student or co-living schemes.

Hub and Bridges said Cornerstone will be the first project in their expanding co-living portfolio that they plan to build and hold. Other sites include the pair’s first investment in Hammersmith and Fulham.

Damien Sharkey, managing director at Hub, said: “Not only is Cornerstone our first co-living scheme in the City of London, but it is the first asset within our ultra-urban co-living portfolio that Bridges and Hub plan to retain beyond practical completion and operate. We see enormous potential in the sector and its role in shaping the future of urban living.”

With strip-out of the existing building complete and enabling works under way, construction is expected to start following Gateway 2 approval. Practical completion is slated for 2028.

Victor Librae, chief executive at Firma Partners, said: “The structure of this facility has been designed to align with the realities of delivery and leasing in today’s market, while providing the sponsor with the flexibility needed to navigate the complexities of the Gateway system.”

BBS Capital advised the parties in securing debt, with JJ Rhatigan appointed as main contractor.

Criterion Capital secures £294m loan for West End acquisitions

Facility to support purchase of St Giles London hotel and refinance Haymarket House

What: Asif Aziz’s Criterion Capital has secured a £294m loan from Maslow Capital

Why: Facility will refinance Haymarket House and support the acquisition of St Giles London hotel

Whatnext: Haymarket House will be converted into a 508-bed Zedwell

Billionaire investor Asif Aziz’s Criterion Capital has completed a £294m financing agreement with Maslow Capital.

The loan will support the firm’s acquisition of the St Giles London hotel and refinance Haymarket House, through a bespoke construction facility to convert the building into a 508-room Zedwell hotel.

BBS Capital acted as exclusive adviser to Asif Aziz and Criterion Capital on the transaction.

Joanne Barnett, co-founder of BBS Capital, said: “Our role was to advise Asif Aziz and Criterion Capital to bring the right capital partner to the table for a multi-asset, prime central London hospitality and retail transaction.

“The structured facility was executed in short order with thanks to the professionalism of all parties involved, including the legal teams at DLA (for the lender) and Deloitte (for the borrower). Maslow’s continued ability to provide complex bespoke facilities provided a strong fit for the borrower.”

Aziz completed the £220m acquisition of the St Giles London hotel from IGB Corporation Berhad, as first tipped by Green Street News. The deal for the 732-room hotel marks one of the biggest hospitality transactions in the UK, equating to £300,000 per room.

The high-net-worth investor purchased Haymarket House at the end of 2023 for £135m. The West End development has been earmarked for a hotel conversion by previous owners CPPIB and Hermes Investment Management.

Aziz, founder of Criterion Capital, said: “This facility supports the acquisition of St Giles London hotel and the delivery of Haymarket House – two key assets within our West End hospitality portfolio, which now comprises 3,700 operating rooms and a target of reaching 9,000 by 2029.

“The structure provides the flexibility we need to continue executing our plans across the portfolio, and we appreciate the support of Maslow Capital and the advice of BBS Capital throughout the process.”

Adam Baghdadi, head of lending solutions at Maslow Capital, added: “Criterion Capital has a substantial track record in London and the West End hospitality market, and it has been a pleasure to work together on this portfolio transaction.

“The facility supports standing assets while providing flexibility as transformational work progresses. Completing over the holiday period required focus and alignment across all parties. We look forward to building a long-term relationship as the portfolio continues to evolve.”

DLA acted as legal adviser for Maslow Capital, while Deloitte represented Criterion Capital.

Term Sheet: Bayes reveals a UK lending surge, Blackstone’s f507m CMBS is priced, CapitaLand targets Asian lending

The latest Bayes Business School UK lending report reveals there was a jump in origination in H 1 ; a Blackstone-sponsored logistics CMBS has closed, boosting European issuance volumes; CapitaLand sees the potential in Asian real estate debt markets with latest fundraising drive; and more in today’s briefing, exclusively for our valued subscribers.

They said it

“The debt market righ t now feels as competitive as pre-GFC”

Adam Buchler, managing director at London-based debt adviser BBS

Capital, tells Real Estate Capital Europe margins on stabilised UK assets have

compressed to below 150 basis points amid lender competition.

What’s happening

Quids in

While lenders almost uniformly report a clamour for the best real estate financing transactions, data released today shows refinancing has kept debt providers in the UK busy. The mid-year 2025 UK lending report by Bayes Business School delivered several key takes on the market. Here are three, and full coverage can be found here.

1. Refinancing fuelled a strong HI: At f22.3 billion (€25.6 billion), loan origination was 33 percent higher than in the same period last year. Report author Nicole Lux said the scale of the increase was a surprise, given the subdued transactional market. Of total origination, 74 percent related to refinancing. On the back of the HI performance, Lux expects 2025 to represent a 10-year high for lending.

2. Debt fund defaults increased: In more concerning news, Bayes reported the default rate among debt funds to have risen from 15.2 percent to 20 percent during HI. Lux told REC Europe the jump could be due to debt funds, which have fewer reporting requirements than banks, only now beginning to report defaults.

3. Prime offices are in focus: After a rocky few years, the office sector is back in lenders’ sights – at least prime offices are. Of the lenders Bayes surveyed, 88 percent indicated their willingness to finance prime offices. The report showed competition for the best workspace assets has forced prime margins down from 249bps to 231 bps over HI.

Logistics solutions

A major logistics securitisation, sponsored by Blackstone, priced this week. The E507 million UK Logistics 2025-2 DAC CMBS deal priced with a weighted average margin of 199 basis points over Sonia — 44bps inside the same sponsor’s UK Logistics 2025-1 CMBS in April. The transaction is the securitisation of part of a €760 million loan provided to the US manager by

a banking syndicate comprising Natixis, Societe Generale and Morgan Stanley. The loan is backed by 114 logistics assets operated by Blackstone portfolio company Indurent Management. Natixis and SocGen securitised a portion of their shares of the loan. Logistics financing has been a significant component of CMBS issuance in Europe so far this year. The market is experiencing something of a renaissance, with more than €6 billion of issuance so far this year, across 11 deals. Ratings agency Scope Ratings identified €2.3 billion across the whole of 2024.

Checking in

Lenders are competing to finance prime London hotels, and among them are US managers King Street Capital Management and Apollo Global Management. Last week, the two firms provided a f348 million (€408 million) senior loan to refinance the Park Tower Hotel, a 271 -room property in London’s Knightsbridge area. The upmarket hotel is subject to a

refurbishment plan. Stabilised hotels and development projects alike are attracting financing from a broad range of lenders, per risk management firm Chatham Financial’s Lending Market Overview for Q32025. In September, in its Spotlight: UKHote1 Market 2025 report, property adviser Savills said year-to-date UK hotel investment volumes were down 28.6

percent to €3.01 billion, due to fewer portfolio deals. But a 33.1 percent year-on-year surge in single-asset transactions signalled investment market appetite.

Strike two

Emerging real estate debt managers, in a September article, told RECEurope strategies are stronger with a differentiated mandate. Among them was Redevco, which launched a debt arm in January and seeks out what it sees as sustainable transitional development projects. In its second real estate loan to date, the Dutch manager has backed the delivery of German

logistics developments, owned by US manager Invesco Real Estate and logistics developer Propel Industrial, with a €67 million loan. So far, Redevco’s debt arm has deployed more than €120 million. The firm is aiming to deploy balance sheet capital into senior, whole and mezzanine loans across European markets and asset classes, including acquisition, capex and development financing.

Trending

Look east

Asia’s private real estate debt market lags the US and Europe. However, some managers see potential in raising capital for credit strategies in what has traditionally been a heavily banked region. This week, affiliate title PERE revealed Singapore-based real estate investment management firm CapitaLand Investment is aiming to raise $320 million for the second in a

series of Asia-focused credit funds, with plans for a third already in the works. CapitaLand is aiming to raise the capital from investors hailing from Asia, as was the case with its first vehicle, but also now from Europe, the US and the Middle East. In a February report, PERE explored the growth of Asia’s private real estate debt market. While Australia has taken much of the focus to date, managers are increasingly attracted by a funding gap in markets including Hong Kong and China. Adviser CBRE identified outstanding senior commercial real estate debt in Asia-Pacific of $257 billion, with a funding gap of $8.4 billion expected between 2024 and 2026.

Split opinion

German bank Berlin Hyp polled more than 650 real estate professionals at Expo Real 2025 for its annual Trendbarometer survey, and the findings show the industry is divided on recovery prospects for 2026. Asked when they think transaction market activity will pick up again, 44 percent said they expect it to occur in the coming year, although 36 percent are already

looking to 2027. A more pessimistic 12 percent of respondents expect transaction activity to pick up later than that. “The transaction market is the most important indicator of the state of the real estate sector,” commented Sascha Klaus, chair of the board of management at Berlin Hyp. “The really big transactions are still lacking.” For more on the survey results, see here.

REC Europe Awards 2025

Make your case

Nominations for the REC Europe A wards 2025 are open. As was the case for the 2024 awards, a panel comprised of senior editorial staff will determine the winners and runners up. To ensure the panel has as much information as possible ahead of the decision-making process, you now have the chance to make a case for your organisation, transaction, or yourself being in

contention across our 27 categories. To make a nomination, fill in the form, which can be found HERE by midday, UK time, on Monday 17 November. We look forward to hearing from you.

People

Gellatly on board

London-based manager Precede Capital Partners has appointed industry veteran John Gellatly as its non-executive chairman. He succeeds Nigel Webb, who was interim chairman following the passing of Frank Strauss in May 2024. Gellatly has four decades of experience in real estate. He has held senior global real estate investment roles with investment firms including US manager BlackRock, London-based Aviva Investors and, most recently, the sovereign wealth fund Abu Dhabi Investment Council. In addition, Gellatly is an eminent fellow of the Royal Institute of Chartered Surveyors and has served on advisory panels for the Bank of England and the Property Industry Alliance.

Data snapshot

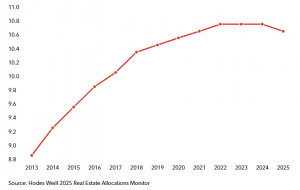

Allocation dip

Institutional investors’ target allocations to real estate have fallen for the first time in at least 13 years, according to the latest Hodes Weill 2025 Real Estate Allocations Monitor. Doug Weill, co-founder of the advisory firm, told affiliate title PERE the drip is very significant, but added: “What I would say is we don’t think institutions are abandoning their allocations to

real estate.” Read PEREs coverage here. Look out for this week’s PERE Podcast for more analysis of the report.

Real estate allocations grew steadily from 2013 to 2021 before leveling off and declining for the first time this year (%)

Dandara and Gamuda secure financing for £80m Glasgow student scheme

Debt adviser BBS Capital arranged the facility

What: Dandara Living and Gamuda Land have secured £43m of financing from Bank of Ireland

for a student scheme at Anderston Quay

Why: Loan will support development of the City Wharf project

What next: Completion is anticipated in time for the 2026/27 academic year

Developer Dandra Living and Malaysian real estate firm Gamuda Berhad have secured financing for a purpose-built student accommodation (PBSA) project in Glasgow, Green Street News can reveal.

Bank of Ireland has agreed a £43m facility to progress the joint venture’s development of City Wharf, which has an estimated end value of £80m.

The financing, arranged by debt adviser BBS Capital, sits at a loan-to-end value ratio of around 54%. The deal also marks BBS Capital’s 10th transaction in the living sector this year.

Mark Geraghty, director of BBS Capital, said: “We are glad to have closed this important financing for our clients Dandara and Gamuda with Bank of Ireland. The transaction – our 10th financing so far this year in the living sector – highlights its attractiveness to both debt and equity investors.”

Upon completion, City Wharf will provide 492 student beds, comprising studios and cluster bedrooms. The site is next to Kingston Bridge at Anderston Quay, and will help to reduce the shortfall of student accommodation in the city.

The scheme marks Gamuda’s first student development outside London and its second PBSA project in the country. It made its UK debut last year through a £100m joint venture with Singapore-based private equity firm Q Investment Partners to develop a 299-bed student scheme in Woolwich, London.

The Glasgow project forms part of Gamuda’s broader PBSA portfolio strategy, which aims to build 3,000 student beds across the UK by 2027.

A representative for the joint venture said: “The construction is well progressed and will soon deliver almost 500 quality PBSA beds into a highly undersupplied market.

“The JV appreciates the efforts of all involved, including Bank of Ireland and its advisers, BBS Capital – bringing an attractive financing package to a successful close.”

Phil Edwards, director of property finance, corporate banking at Bank of Ireland, said: “Supporting sustainable, resilient and future-focused real estate investment, including in the purpose-built student accommodation sector, is a core area of focus for us.

“We are pleased to have provided the financing support for this Dandara and Gamuda joint venture, and look forward to working closely with them and BBS Capital on future projects.”

Dandara Living is acting as developer and contractor for City Wharf, which has begun construction. The scheme will integrate low- and zero-carbon technologies to achieve BREEAM Very Good certification. Completion is anticipated ahead of the 2026/27 academic year.

BBS Capital strengthens leadership with promotions

Kazeem Afolabi, Joseph Clery and Amandeep Uppal take on higher responsibilities

What: BBS Capital has promoted Kazeem Afolabi, Joseph Clery and Amandeep Uppal

Why: Move to further strengthen the real estate adviser’s leadership capabilities

Whatnext: Uppal is appointed as Head of Transaction Management and General Counsel; and Afolabi and Clery as Directors

Real estate finance advisory BBS Capital has made several key promotions to strengthen its leadership capabilities, Green Street News can reveal.

The company has elevated Kazeem Afolabi and Joseph Clery to Director positions, and Amandeep Uppal as Head of Transaction Management and General Counsel.

Afolabi, who has been part of the firm since 2020, has been involved in transactions totalling more than €2bn in financings. He joined from Eastdil Secured and spent six years at Goldman Sachs’ real estate development team, which was behind the delivery of Goldman’s 1.2m sq ft EMEA headquarters.

Clery joined in 2022 and has been instrumental in structuring and securing financing for a number of complex real estate deals across the UK and Europe. He worked at Rivercrown, where he split his time between the capital advisory and principal investment teams, focusing on special situations. He also spent five years at HoH Capital Partners as part of its investment team, and at Queensgate Investments, where he was a member of the acquisitions team.

Amandeep Uppal joined BBS Capital in 2020 as In-House Counsel and is backed by nearly a decade of legal experience at firms include Deutsche Bank, JP Morgan Chase, Mayer Brown and Fieldfisher.

BBS has a 20-year track record advising on both real estate debt and equity finance across all real estate sectors. Headquartered in Marylebone, the company recently completed more than £500m of financing mandates, with a further £1.5bn in the pipeline. These include a £200m joint venture for student accommodation between TPG Angelo Gordon and developer Hollybrook, revealed by Green Street News.

The firm also played a key role in securing an £85m refinancing of a portfolio of hotels next to Manchester airport, tipped by Green Street News in February.

Joanne Barnett, Co-Founder of BBS Capital, said: “Kazeem, Joseph and Amandeep have consistently demonstrated great leadership, ingenuity and a deep commitment to our clients’ success. Their promotions reflect the significant impact they’ve made and the trust they’ve earned across the industry.

“As we continue to grow our presence in the UK and internationally, we will fully support them in their new roles and are confident their expertise will play a vital role in advancing our strategic ambitions.”

BBS Capital is led by Managing Director and Co-Founder Adam Buchler, alongside Joanne Barnett and Nick Spencer.

Canada Life AM refinances Global Gate’s Mayfair office

30,000 sq ft Maddox Street asset was bought in 2020

What? Canada Life has provided a £35m loan to refinance Global Gate’s 25 Maddox Street in Mayfair

Why? The previous facility put in place in 2020 matured

What next? Office take-up in the West End in the first quarter was up by 11% on the five-year average

Canada Life Asset Management has provided a £35m senior facility for a prime London office owned by Global Gate Capital, Green Street News can reveal.

The freehold five-storey 25 Maddox Street office comprises around 30,000 sq ft of lettable space. The loan supports Global Gate’s long-term strategy for the asset, which it acquired in an off-market transaction in late 2020.

Nicholas Bent, head of real estate finance at Canada Life AM, said: “This is a well-specified building in one of London’s most resilient office sub-markets. We are proud to support institutional borrowers in acquiring and holding high-quality assets over the long term and look forward to developing a lasting relationship with Global Gate as they continue to grow and succeed.”

Take-up in the West End office market has remained resilient in the first quarter of the year, according to real estate consultant Savills. Some 474,638 sq ft transacted in March, bringing the total for the quarter to 755,551 sq ft across 86 transactions – up 20% on Q1 2024 and 11% on the five-year average.

Iain Bond, senior adviser at Global Gate, said: “The building is exceptionally well located and reflects our continued conviction in the West End office market, particularly for high-quality assets with strong fundamentals.”

Real estate consultant BBS Capital structured and arranged the financing for the sponsor.

Kazeem Afolabi, associate director at BBS Capital, said: “This transaction reflects the strength of the asset, sponsor, and lender relationship. Despite ongoing volatility in the wider market, demand for well-located, income-producing assets remains firm.”

Firma backs Tribeca’s Brompton Cross redevelopment plans

New lender’s third loan supports residential-led scheme at 90 Sloane Avenue

What? Firma Partners has provided a whole loan to support Tribeca Holdings’ planned redevelopment of 90 Sloane Avenue

Why? Debt will help fund the redevelopment of the building into a 24-home scheme

What next? Planning authorities are to decide on application

Firma Partners is providing financing for Tribeca Holdings’ planned redevelopment of 90 Sloane Avenue, Green Street News can reveal.

The lender, which launched earlier this year, is advancing a whole loan to support Tribeca’s plans for a six-storey luxury residential scheme with a ground-floor retail unit.

The loan amount was not disclosed, but is understood to be in the region of £30m.

Located opposite the Bibendum building at Brompton Cross, 90 Sloane Avenue is currently a five-storey building comprising 20 apartments and ground-floor retail space, let to fashion brand Joseph.

Octopus provides £33m for Cheltenham town centre redevelopment

Octopus Real Estate has completed a £33m facility for redevelopment in Cheltenham town centre.

The funding has been provided to Wavensmere Homes and Montane Partners for their £50m redevelopment of the North Place surface car park.

This site will host Arkle Court, a 3.5 acre development comprising 147 houses and apartments.

Arkle Court is the most central residential development in Cheltenham and received a resolution to grant planning in August 2024.

Site enabling works began in February 2025 with groundworks to commence in April.

Construction of the 75 three-bedroom townhouses and 72 one and two-bedroom apartments is anticipated to take two and half years to complete, with the first handovers scheduled for Q3 2026.

The scheme has been designed by architects Glancy Nicholls to complement the town’s Regency architecture.

This financing was arranged by debt advisory boutique BBS Capital, and marks the third time Octopus Real Estate and Wavensmere have teamed up in recent years to deliver a brownfield regeneration.

“At Octopus Real Estate, we always want to work with best-in-class developers who are aligned with our vision and values,” said Sam Wisker, investment manager (commercial and development debt) at Octopus Real Estate.

“Wavensmere has a strong reputation for delivering high-quality, sustainable homes. We are thrilled to be once again working with this dynamic team, and look forward to seeing the positive impact the Arkle Court regeneration project will have on the local area.”

James Dickens, managing director of Wavensmere Homes, added: “While we are already on site, this funding facility enables us to confirm delivery timescales.

“The quality of our Arkle Court development will showcase what can be achieved when the Borough Council and developers work together to unlock complex regeneration schemes for the benefit of Cheltenham.

“Our team will continue to work with the Council and other stakeholders as the construction programme progresses.”

Israeli lender refinances £135m Manchester airport hotel portfolio

Facility secured against three hotels next to Terminal 2

What: Bank Hapoalim has provided an £85m refinancing package for a portfolio of three hotels next to Manchester airport

Why: The facility replaces a development loan from ICG Real Estate

What next: The three-year loan is due to mature in 2028

A joint venture between high-net-worth investors and Scala Capital has secured an £85m refinancing of a portfolio of hotels next to Manchester Airport, Green Street News can reveal.

The three-year loan from Israel-based Bank Hapoalim is secured against the 280-room Holiday Inn, the 262-room Ibis and the newly opened 412-room Tribe – Manchester’s largest hotel.

Green Street News understands that the facility, which has been originated at around 60% loan-to-value, replaces a development loan previously provided by ICG Real Estate.

Benny Haddad, managing director at Bank Hapoalim, said: “Scala Capital has developed a high-quality hospitality portfolio in the UK’s second-largest airport. The strong and stable cash flow dynamics of these assets make them a compelling fit for our senior financing.”

Scala Capital was advised by BBS Capital and CMS, while Bank Hapoalim was advised by Baker Mckenzie.

Joanne Barnett, co-founder at BBS Capital, said: “The competitive financing process underscored the strength of the sponsor and the quality of the assets. Bank Hapoalim’s flexible and pragmatic approach made them the ideal lending partner, and we are delighted to have closed this transaction to kick off 2025.”

TPG Angelo Gordon secures £200m debut for student JV

New partnership aims to provide 2,000 beds in next three years

The joint venture is seeded with a 271-bed student project in Wimbledon

What: TPG Angelo Gordon has partnered with Hollybrook for a new student joint venture

Why: Joint venture aims to secure opportunities in supply-constrained student markets across the UK

What next: Second London site due to be acquired in the coming weeks

TPG Angelo Gordon has teamed up with developer Hollybrook for a new joint venture, targeting the acquisition and development of 2,000 student beds over the next three years, Green Street News can reveal.

The platform will target supply-constrained, multi-university UK student markets with growing student populations. It is aiming to acquire, build and stabilise the assets over the next five years.

The partnership has seeded the platform with a 271-bed development on Kingston Road, Wimbledon. The purpose-built student accommodation (PBSA) scheme is already under way and is due to be completed ahead of the 2026/27 academic year, providing beds for students at Wimbledon College of Arts.

A second site in London has also been secured. It comprises 300 student beds, with the two debut schemes having a combined development value in excess of £200m.

In addition to the pair of London sites, the joint venture has a pipeline of both operational assets and development sites, for which it is looking to secure planning permission for more than 1,000 PBSA beds in 2025. The joint venture will also work directly with Hollybrook’s construction business to deliver the projects.

Hollybrook is a family-owned developer and construction company. It has developed 5,000 homes, with a further 7,000 in planning – including schemes across Southwark, Barking and Havering.

Other projects on its books include a £500m residential-led development in Neasden, which is to include more than 1,000 homes, 600 student beds and around 120,000 sq ft of industrial space.

Valerie Cox, director of Hollybrook, said: “We are delighted to be working with such a well-respected partner in TPG Angelo Gordon, and look forward to acquiring a significant number of PBSA development sites within the next couple of years. We see significant demand from students for PBSA and we are delighted that TPG Angelo Gordon share our vision and are investing alongside us in this sector.”

John Parsons, vice president at TPG Angelo Gordon, added: “We are excited to close the first in a series of transactions with our new student accommodation partner, Hollybrook. This transaction exemplifies our strategy of targeting supply-constrained student locations in the UK, providing beds for both domestic and international demand.”

TPG Angelo Gordon remains active in the student market across Europe, and recently secured finance for a £150m student scheme in Bristol that it is delivering in a joint venture with Melburg Capital.

What Federated Hermes has provided Silverpeak with a £55m loan

Why To refinance a trio of Mayfair office assets

What next Previous lender Citi will be paid back

Silverpeak Asset Management has refinanced a trio of Mayfair office buildings with a new £55m facility provided by Federated Hermes, Green Street News can reveal.

The UK investment arm of the Ruimy family office has secured the debt to refinance an existing loan from Citi held against both 47-48 and 49 Grosvenor Street as well as 28 Savile Row. The three assets have been held within the family’s ownership for over a decade.

The loan, which was arranged by BBS Capital, sits at a loan-to-value of 60%, meaning the three assets are valued at around £91.7m. The new facility will allow the owners to “advance plans for the portfolio”.

“Strong and stable”

David Goldenberg of Silverpeak Asset Management, said: “We are excited to partner with Federated Hermes Private Credit whilst executing our business plan on the portfolio and capitalising on opportunities in the market. BBS Capital’s expertise and support were key to achieving this successful outcome.”

Vincent Nobel, head of asset-based lending at Federated Hermes, said: “Silverpeak Asset Management has built an established portfolio of high-quality assets in core West End locations which provides strong and stable cash flow dynamics for the senior financing we are providing.

“As we begin 2025, investors are continuing to use real estate debt as a key diversifier in their real asset portfolios, which requires stability of income distributions from real estate debt investments in the face of the evolving real estate market.”

Adam Buchler, managing director at BBS Capital, added: “The financing process we ran was highly competitive given the quality of the assets and the strength of the sponsor. Federated Hermes Private Credit was selected due to their flexible and pragmatic approach to the sponsor’s business plan, and it was a pleasure working with them and all parties involved to close this financing over the Christmas period.”

What – Forma Real Estate has secured a £12.5m loan from Santander

Why – Loan is for its 40 Villiers Street property in central London

What next – Fund manager plans to carry out further asset management initiatives

Forma Real Estate has secured a £12.5m loan from Santander on its 40 Villiers Street asset in central London, Green Street News can reveal.

The property, prominently located on the corner of Embankment Place and Villiers Street, was acquired by Forma from ARA Dunedin in October 2023 for around £26m.

Since acquisition, Forma has completed two ground-floor retail lettings and one office-floor letting. It has also invested into the asset, with the addition of an enhanced roof terrace overlooking the River Thames.

Chris Taylor, chief executive of Forma’s UK team, said: “We have had a really positive 12 months completing a number of the asset management opportunities we had identified prior to purchase.

“Having stablised the property with these successes, now was the appropriate time to seek a debt financing, and we are delighted to have secured the support of Santander as we progress further initiatives for the asset.”

Greg Martin, director of real estate finance at Santander, corporate and commercial, added: “We are pleased to have provided Forma with a £12.5m lending package. The firm’s plans for enhancing its Villiers Street property will create new opportunities and will support further growth. We look forward to continue working with the Forma team.”

Forma was represented in the transaction by BBS and Fladgate. Pinsent Masons advised Santander.

Other transactions for Forma this year have included the purchase of 19-31 Piccadilly, a mixed-use asset opposite Piccadilly Gardens in the centre of Manchester, which was acquired from L&G in a £24m deal.

ASK provides debt facility for Elephant and Castle development site

ASK Partners has provided a senior loan facility to the joint venture between residential property development company HUB, and global investment firm, H.I.G. Capital, in a deal brokered by BBS Capital.

The facility supported the JV’s recent acquisition of a cleared 1.2-acre development site in central London.

The site is the final parcel of undeveloped land on the Elephant Park masterplan site at Elephant and Castle and benefits from outline planning permission for a residential development.

The JV plans to seek permission for a residential-led scheme of significant scale including shared-living homes, affordable homes, new public realm, ground floor retail provision and a health hub.

The masterplan has to date delivered 3,000 homes, with more coming to market in 2025, and 150k sq.ft. of retail, plus an improved underground station and a new University of Arts London campus.

Miles Keeley, head of acquisitions at HUB, said: “This deal is part of our ongoing strategy to build a portfolio of assets in the living sector in ultra urban places, targeting central London and other key regional cities.

“This is our second deal with H.I.G. and our third financing with ASK, with whom we have developed a strong working relationship.

“We were pleased to work with both counterparties on this transaction and we look forward to being custodians of this incredible site.”

Elliot Blatt, head of origination at ASK, said: “We are delighted to be working with HUB and H.I.G. again, their strategy very much resonates with our underwriting approach.

“Having bought the site for £42m, potentially under market value, the JV has injected significant equity into the project putting ASK’s loan at a sensible loan to value.

“The partnership has a strong track record and this is an excellent development site.

“It is a great option for a residential-led strategy given the area’s strong transport links and the considerable inward investment into its housing, retail and public realm supply over the last 10-15 years to transform it into a desirable hub for living.”

Adam Buchler, partner at BBS Capital, added: “It was a pleasure to complete another financing for our clients H.I.G Capital and HUB and to continue to build on our relationship with ASK with whom we’ve worked on a number of important development propositions.

“The site presents a strong investment opportunity and we look forward to seeing plans come to fruition.”

Melburg and TPG bank finance for £150m Bristol student scheme

Joint venture to provide 399 student beds in South Plaza project

CGI of the proposed Bristol student scheme

What: Melburg Capital and TPG Angelo Gordon have secured a development finance facility from Maslow Capital Why: To finance their South Plaza scheme in the centre of Bristol What next: £75.5m facility will help deliver 399 student beds

A joint venture between Melburg Capital and TPG Angelo Gordon has secured a £75.5m development finance facility with Maslow Capital for a student scheme in central Bristol, Green Street News can reveal.

The finance package will help to bring forward the joint venture’s South Plaza project, which will include 399 student beds.

Planning permission was secured to repurpose the former office building into student accommodation in May this year. Contractor Winvic is in place to build the scheme, which is understood to have a gross development value in excess of £150m.

Melburg and TPG’s plans involve retaining the building’s original structure, saving 4,215 tonnes of embodied carbon compared with a demolition and rebuild.

The project will also be connected to Bristol’s district heat network and is targeting BREEAM Excellent and EPC A ratings.

“We continue to selectively grow our student housing exposure as part of our wider investment into the living sectors” – Jack Burgess, Melburg Capital.

The project will also offer nearly 11,500 sq ft of internal amenity space, with features including a yoga studio, gym, lounge, library, meetings rooms and a roof terrace. The joint venture is targeting completion in June 2026, ahead of the 2026/27 academic year.

Burgess Okoh Saunders and Freedman + Hilmi provided legal services. Savills acted as property adviser. BBS Capital acted as debt adviser to the joint venture.

Jack Burgess, chief executive at Melburg, said: “We are pleased to be working with Maslow Capital on this ambitious project and look forward to welcoming students in the 2026 academic year. We continue to selectively grow our student housing exposure as part of our wider investment into the living sectors, which now stands at over 2,500 beds.”

James Henry, origination director at Maslow Capital, added: “Maslow is delighted to be partnering with Melburg to deliver much-needed student housing in the Bristol market. This £75.5m commitment underscores Maslow’s strong appetite for partnering with best-in-class sponsors and delivery teams to fund high-quality living sector assets across the UK and Europe.

“It has been a pleasure working with all parties involved, and the Maslow Capital team looks forward to seeing the asset’s delivery over the next two years.”

Melburg’s blockbuster fundraise

The scheme follows a significant fundraise by Melburg, which secured £565m for its debut UK real estate fund in May this year. Melburg Real Estate Fund I (MREF I) will invest both directly and in joint venture opportunities, and has been backed by several of the investment manager’s existing institutional partners along with private family offices.

The deal is the latest significant investment in the Bristol student market, which continues to record rising demand and a shortage of space.

Earlier this month, Green Street News revealed AustralianSuper had made its debut in the UK’s PBSA market, with a forward-funding deal for a £120m project in the city being brought forward by Avon Capital Estates.

The Bristol deal is expected to be a blueprint for how AustralianSuper builds its UK student business, with the focus to be on funding and development opportunities, as well as buying top-quality existing operational assets.

BBS Capital introduces £100m in business to Octopus Real Estate in 2024

Real estate finance adviser BBS Capital (BBS) today announces the successful completion of over £100m in financings with specialist property lender and investor Octopus Real Estate during 2024.

This accomplishment is particularly meaningful given the challenging economic landscape and conditions affecting the commercial property market in recent years, and particularly highlights the strength and resilience of a long-standing working relationship between BBS and Octopus Real Estate.

BBS has introduced high-quality financing opportunities across a range of sectors and regions, with notable successes in the residential, student accommodation, and industrial markets.

With further loans in the pipeline for 2025, this partnership continues to support projects that contribute meaningfully to the ongoing regeneration of the UK property landscape.

James Nunn, Investment Director, Octopus Real Estate:

“We thoroughly enjoy working with the team at BBS Capital. Their meticulous due diligence and high-quality loan delivery make the underwriting process swift and efficient, which has been especially valuable in today’s market.”

Joanne Barnett, Co-Founder, BBS Capital:

“The strength of our relationship with Octopus Real Estate, built over many years, is a key factor in surpassing £100m of completed loans this year.

We have no hesitation in recommending Octopus as a funding partner; the success we have had together in 2024 has set the stage for continued growth and innovation in UK property financing in 2025.”

Crosstree and Bloom secure £29m loan for industrial estate repositioning

West London asset is first in duo’s new venture

What Birchwood has provided Crosstree and Bloom with a £29m loan

Why To finance the acquisition and repositioning of Fairview Business Centre

What next A comprehensive refurbishment will be undertaken to modernise and upgrade its EPC rating from D to A+

Birchwood Real Estate Capital has provided a £29m loan to finance the acquisition and repositioning of Fairview Business Centre in Hayes by Crosstree and Bloom, Green Street News can reveal.

The quantum of the finance held against the asset, which was bought for £30m for A2 Dominion Group, represents 55% of its projected stabilised value. The loan from the WR Berkley-backed financier includes a substantial capex tranche, with Bloom and Crosstree aiming to carry out a comprehensive refurbishment of the estate and improve its EPC rating from D to a targeted A+ rating.

Lorna Brown, founder of Birchwood, said: “We are delighted to have supported Bloom and Crosstree on the financing of the first acquisition of their urban logistics JV and to have provided capex facilities which will enable the repositioning of Fairview Business Centre to deliver high-quality modern warehouses in key London locations. It has been a pleasure to collaborate again with BBS in delivering thoughtful financing solutions for high quality sponsors.”

Adam Buchler, managing director of BBS Capital, which advised the borrower, added: “In the current market with transaction volumes lower than usual, the debt markets are extremely competitive for strong projects like this with a high calibre sponsor, well located real estate and robust business plan. Birchwood were selected not only for their competitive commercial terms but also for their flexibility and speed of execution.”

Asif Aziz’s Criterion secures £25m facility for Zedwell hotel expansion

Loan was provided by specialist lender Cynergy Bank

What Criterion Capital has secured a £25m investment facility from specialist lender Cynergy Bank

Why Funding intended to boost the Zedwell brand’s UK-wide expansion

What next Zedwell is set to expand its portfolio to 8,000 rooms by 2027

Criterion Capital, the property firm controlled by billionaire Asif Aziz, has secured a £25m investment facility from FSCS-registered specialist lender Cynergy Bank for the expansion of its Zedwell hotels portfolio.

With three central London locations already, Criterion said the facility will help the brand’s growth across city sites in the UK.

Upcoming Zedwell hotels will soon debut in cities including in York, Manchester and Edinburgh.

In August the property firm, which was advised by BBS Capital, also secured a three-year £25m loan from the Bank of London and the Middle East (BLME). The funding was intended for the conversion offices on London’s Trafalgar Square into a Zedwell hotel.

Criterion launched its first Zedwell property in London’s Piccadilly in 2020 after almost eight years of delay. The second hotel under the brand opened in Tottenham Court Road later that year, as the capital’s first underground hotel.

Zedwell offers rooms named “cocoons”, which features soundproof walls, floors and doors, hypnos mattresses, purified air and warm ambient lighting.

With 13 new sites in development, Zedwell is set to expand its portfolio to 8,000 rooms by 2027.

Omar Aziz, director at Criterion Capital, said: “This £25m equity release is pivotal in accelerating the Zedwell brand’s UK-wide expansion. We are looking forward to turning prime sites in cities across the UK into vibrant and thriving hospitality assets.”

Nishil Tanna, relationship director at Cynergy Bank, added: “We are glad to partner with Criterion Capital on this transformative journey. Their vision for Zedwell aligns perfectly with our commitment to supporting growth and we look forward to seeing their continued success as they bring Zedwell to some of the UK’s most iconic locations.”

Law firm Harold Benjamin represented Criterion Capital on the deal.

Loan to PineBridge Benson Elliott has an LTV of 72.5% while deal with Metrobox carries an LTV of 53%

What M&G Real Estate has agreed £200m of refinancing deals in the retail warehousing and logistics sectors

Why Firm provided a £50m construction loan to PineBridge Benson Elliot and a £150m facility to Metrobox

What next Loan to PineBridge has an LTV of 72.5% while deal with Metrobox carries an LTV of 53%

The finance team of M&G Real Estate has agreed to provide £200m of refinancing across two transactions within the logistics and retail warehousing sectors.

M&G has lined up a £50m construction loan to PineBridge Benson Elliott for the ongoing development of two logistics properties in Woodford and Enfield, north London. Both sites have planning consent for seven warehouse units totalling 175,000 sq ft, with completion aimed within 18 months. The facility has a loan-to-value ratio of 72.5%.

The second transaction is a £150m refinancing deal with Metrobox, an urban retail warehousing joint venture between Delancey and Tritax. The loan will refinance an existing debt facility secured against four retail warehouses located in Guildford, Crawley, Luton and Solihull. The units are let to tenants including Next, B&Q, Halford, Marks & Spencer, Argos, Sports Direct, Pets at Home and

B&M. The loan has an LTV of 53%.

George MacKinnon, managing director of PineBridge, said: “PineBridge has completed this financing with M&G, which enables the development of two high quality, sustainable urban logistics assets in core central London sub-markets where they are much needed to satisfy the needs of modern occupiers. We look

forward to working with the M&G team in delivering the assets.”

Adam Buchler, managing director of BBS Capital, which advised PineBridge, “We’re delighted to have acted for Pinebridge on

this financing as part of our continued drive into the logistics sector. The M&G team adopted a refreshing and pragmatic approach throughout the process and we look forward to working them on other transactions going forward.”

A spokesperson at MetroBox, said: “Despite the refinancing exercise being undertaken during an uncertain time in the debt market, we were pleased to see significant interest from lenders. It has been great to work with the team at M&G who provided competitive terms. This deal stems from the high quality of the assets and the asset management successes of Delancey and Tritax on our MetroBox JV.”

M&G Real Estate’s finance team has deployed over £13bn across the UK and Europe on behalf of more than 100 institutional investors since its establishment in 2009.

Dan Riches, head of real estate finance at M&G Real Estate, said: “We are committed to financing prime logistics and retail warehousing assets in strategic locations in the UK and Europe which meet the evolving needs of modern businesses. Growth in manufacturing and e-commerce are driving demand for grade A logistics space and our focus remains on supporting this uptick in

sentiment through investments on behalf of our clients that are secured against well-located assets.”

Borrowers are increasingly seeking advice from those who are in the market day in, day out

It’s a fine time for debt advisers. As markets have grown choppier, borrowers are increasingly turning to specialists for advice.

This is the culmination of a long-term trend as the prevalence of debt advisers has been slowly increasing since the financial crisis. They were already popular in the US, where the vast majority of the market is now thought to be brokered.

Tougher markets, changing regulations and a growing number of lenders have made them more popular in the UK and Continental Europe. Rising interest rates, collapsing valuations and market liquidity are also factors since, with lending criteria seemingly changing on a daily basis, it pays to have someone who is in the market day in, day out.

The proportion of transactions using advisers is a matter of debate. One market participant put the proportion as high as 60-65%. “There aren’t many deals in the market without a debt adviser,” said another.

The desire to seek out advice when times get tough is understandable. When interest rates first went up and the office market collapsed in the US, it became difficult to know who was open for business and who was keeping things quiet and waiting for the dust to settle. Borrowers are often reluctant to send over opportunities to people who are known to be closed to new business as they don’t want to share sensitive information unnecessarily. That is where debt advisers come in.

Given the number of processes many advisers run, they spend all day in the market getting terms from lenders. This means that if one lender is quoting particularly aggressively, they should be the first to know. It also means that they know more about how lenders are structuring transactions, whether they’re using back leverage, and what covenants they’re asking for. All of this means that advisers should be able to help structure the transaction to make it attractive to lenders before their analyst even opens up PowerPoint to make the deck.

Rothschild & Co advised on the refinancing of SGS, which owns Lakeside in Essex

Given the speed with which interest rates have risen, many borrowers are faced with a refinancing gap which means that they cannot borrow as much as they did previously. When it comes to refinancing, this creates problems, particularly if they are unable to put additional equity in. In these situations, advisers are useful as they can help restructure the capital stack. On a more day-to-day level, debt advisers also help deal with Q&A and the general process management. With processes taking longer, this removes a lot of administration from people’s plates.

However, there are significant differences between advisers, with different firms focusing on different parts of the market from small deals for private clients through to bond issuances for large public companies. There are now a plethora of debt advisors including specialist boutiques as well as divisions within agencies, banks and other service firms. New firms are continually being set up.

Here we profile some of the more active players in different parts of the market and how they are positioned.

Rothschild & Co

Headed up by Toby Cohen and Caroline Kracke in London, Rothschild often deals with the larger and more complicated end of the spectrum. The team advises a range of clients, from public companies to private companies, funds and sovereign wealth funds. Transactions also vary from secured to unsecured, including loans, public bonds and private placements.

The team also has boots on the ground in Paris, Frankfurt, Madrid, Milan, Warsaw, Stockholm and CEE. The European team typically advises on 30-35 financings per year, raising €10bn-15bn of debt.

The average financing advised on is at the larger end of the spectrum at €300m-400m, though the team also works on some smaller single asset financings of below €100m and the largest current refinancing mandate is about €2.5bn.

In Germany, the team led by Henning Block and Hannes Mungenast has been involved in Adler, Corestate, Accentro and Demire

In France, the team led by Arnaud Joubert and Vincent Danjoux have been actively advising AccorInvest on their €4.6bn maturity extension and the restructuring of Orpea

Eastdil Secured

Eastdil also works on large deals. European debt volumes are typically upwards of €18bn a year across sectors.

In Europe, it has offices in London, Frankfurt, Paris, Dublin and Milan. The team is working on a range of deals, from a £50m logistics loan up to a circa £3bn living loan. The team say they speak to well over 100 global lenders a week.

Eastdil is also very active advising on sellers on investment deals, with the debt team working with the equity team on transactions.

JLL has been expanding its offering over recent years. It has also been hiring to fuel the expansion, poaching Stephen Morita from Eastdil and Max Borchert from Cushman & Wakefield to lead the charge in the Benelux region. They also hired Dominik Rüger from Eastdil to help grow the business in the DACH region.

The team, which is led by Brad Greenway and Edward Daubeney, generally closes around 100 transactions a year and currently has $12.3bn of mandates in the market. Since 2018, the team has closed 490 financings with 155 lenders across 20 European markets.

They focus on a wide range of deals, including smaller ticket sizes, which they say gives them valuable knowledge when it comes to the syndication market. The average ticket size is £150m, though they do deals as small as £15m and as large as £2bn-plus.

JLL also has a derivatives advisory team which works alongside the debt advisory team to assist with interest rate and cross-currency hedging solutions.

Recent deals include:

Advising a Cain-led consortium on a £124m debt package for The Stage in Shoreditch

Running the refinancing process for the Langham Estate, securing a £500m financing package from Ares

The team at CBRE, led by Chris Gow, has completed 22 deals, placing £2.8bn of debt over the course of the first half of the year. The average transaction size has increased this year, reaching £127m compared to £58m last year.

The team, which counts 45 people in 10 countries, is currently advising on a range of refinancings and acquisitions, closing two office acquisition loans in London and Amsterdam in the first half of the year.

Brotherton operates in the mid-market space, with an average ticket size of £50m, though it advises on transactions up to £210m. The team specialises in debt advisory only, offering advice across the financing spectrum.

The team kept busy last year, closing around £1.5bn of deals and they expect to close around £2bn this year.

Recent deals include:

Securing a £200m loan from HSBC to support two build-to-rent assets in east and west London owned by Invesco

BBS plays in the mid-market, catering to a variety of high-net-worth individuals and, increasingly, private equity firms. It specialises in loans ranging from £10m to £250m.

The team, which is led by Joanne Barnett, Adam Buchler and Mark Geraghty, has advised on a range of assets, including living, logistics, hospitality, retail and office.

The team has closed in excess of £600m of financings since the start of 2024, with loan sizes ranging from £11m to £78m. They have a further 35 live mandates and are projected to achieve £2bn of financing by the end of the year.

ASK lends £11.7m for residential redevelopment site in Cricklewood

Specialist property lender ASK Partners has provided an £11.7m loan to property investment and development company Ziser London.

The 18-month loan facility is secured against a single-storey retail warehouse, currently let to Matalan, and set on a 2.2-acre freehold site on Cricklewood Broadway, close to Hampstead Heath and the Brent Cross shopping centre.

The loan facility has been provided to refinance an existing lender and allow Ziser London more time to complete the pre-construction phase ahead of implementing the consented planning permission for a 239-bed build-to-rent scheme.

Guy Ziser, director at Ziser London, said: “We always take a long-term view on an asset’s growth potential and working with ASK has given us the flexibility to be able to take a view that will enable this asset to reach its full potential in terms of value.”

Elliot Blatt, head of origination at ASK, added: “This is an excellent redevelopment site and is a great option for a residential strategy given its location and size.

“This transaction brings ASK’s loan book to £1bn, a milestone we’re very proud of, particularly in such challenging economic times.

“We believe our flexibility as a lender is what has enabled us to continue lending through the cycle by backing well-capitalised borrowers with creative strategies which look to respond to the fast-paced change in demand for UK real estate.”

This deal was brokered by BBS Capital and ASK was advised by Fladgate and Montagu Evans.

Milton Keynes’ Station House opens doors to 200 residential units following £35m loan

A former office building in the heart of Milton Keynes, that has been transformed into a new 200-unit residential development, has been refinanced following a £35m residential investment loan from Secure Trust Bank (STB) Real Estate Finance

Located directly above Milton Keynes Central station, Station House is the result of a conversion of disused offices into 200 vibrant apartments across four floors.

Developed by New York and Bahamas-based real estate specialist, Gold Wynn Group, the scheme is one of the latest property developments in an area predicted to see one of the highest long-term growth rates among UK cities outside London. Having topped the UK Competitive Index for 2023, the development will provide much needed housing at a time when demand is on the rise.

The deal for the three-year residential investment loan, agreed at 59% loan to value (LTV), was led by Mike Feasey, Relationship Director at STB Real Estate Finance, alongside Matthew-Blaine Young, the bank’s Head of Origination. BBS Capital advised on and secured this facility for Gold Wynn, continuing its high level of activity in the refinancing space.

Mike Feasey commented: “It was a pleasure to be able to deliver this transaction on behalf of Secure Trust Bank and showcase many of the bank’s strengths. Our hands-on-approach and team ethos, coupled with a strong working relationship with our professional partners, ensured we were able to deliver on a complex transaction in a relatively short period of time. The success of this deal shows what it truly means to be a relationship-led bank and I look forward to building on this success with Gold Wynn over the years to come.”

Taking no longer than an hour to reach London from Milton Keynes Central station, the development is particularly ideal for commuters working, but not living, in the capital.

Ben Friedland, President of Gold Wynn’s US & UK real estate divisions, said: “We’re delighted to have now opened the doors to Station House’s 200 stylish apartments. Milton Keynes is a thriving area on the rise and Station House is proof of this. As experts in property finance, the tailored approach provided by STB ensured that we were able to seal the deal against the clock, proving it to be one of the quickest refinances we have been involved in.”

The bank’s longstanding relationship with BBS Capital, was crucial to completing the process within an allotted timeframe of three months, with it taking just six weeks from sanction to drawdown.

Mark Geraghty, Director at BBS Capital said: “BBS Capital is pleased to have supported Gold Wynn on this key refinancing and build on its relationship with Secure Trust Bank. This was a notable transaction in the office-to-residential conversion space, demonstrating good liquidity in the marketplace for quality assets with robust business plans and credible sponsorship. The structured finance was arranged and executed over a short timeframe despite current market conditions, which is testament to all parties involved.”

Matthew-Blaine Young added: “It was a pleasure to work alongside BBS Capital once again; this deal is the latest of several success stories we have achieved together. As a result, BBS Capital was confident of our ability to provide the necessary property investment finance and deliver on a significant deal associated with unique challenges.”

Acting on behalf of the bank for this property finance loan was solicitors Shepherd & Wedderburn, while BNP Paribas was the appointed valuer for the deal. Both parties played a vital part in organising the deal, alongside Secure Trust Bank’s experienced Relationship Support Specialist, Julie Percy.

Construction has started at The Lampworks, Birmingham-based property developer Cordia UK’s latest project and inaugural Build to Rent development in Birmingham.

Cordia UK has appointed Shropshire-based construction management practice buildfifty5 to deliver the main construction works for the project in partnership with residential general contractor Pedrano UK.

“Buildfifty5 is delighted to be partnering with Pedrano UK on the delivery of The Lampworks in the Jewellery Quarter. Our appointment as construction manager and delivery partner brings together buildfifty5’s core strengths as an organisation focused on collaborative and practical solutions for our key sector clients.”

Garry Whiting, Managing Director, buildfifty5

Construction at The Lampworks is being supported by Cordia International’s key strategic partner – Pedrano Group. With 15 years of experience in apartment developments across Europe, Pedrano will work closely with local contractor buildfifty5 to provide strategic direction on the project.

“At Pedrano Group, we have a long track record of delivering high quality apartments for Cordia International in Central Europe. We are thrilled to be working with Cordia UK to deliver their first Build to Rent development in Birmingham and will be supporting the project strategically from start to finish.”

Gábor Szulyovszky, CEO, Pedrano Group

The Lampworks scheme will deliver 148 Build to Rent homes in a mix of one-, two- and three-bedroom apartments and affordable homes. It will also feature contemporary commercial units on the ground floor, set in a series of striking landscaped courtyards.

Amenities include a co-working space, individual meeting rooms, a shared lounge, and a communal kitchen/diner fit out with modern designs and the latest technologies.

Residents will also benefit from nearby amenities such as Tesco, Morrisons, and popular restaurants and bars including Hockley Social Club and The Church Pub. The scheme is also a five-minute walk from St Paul’s tram stop and ten minutes from Snow Hill train station.

The Build to Rent development is set to be one of the most energy-efficient projects in Birmingham offering exclusively A and B EPC-rated dwellings. The energy efficiency ratings will benefit both future residents and the building operator.

“The Lampworks is the first development in our Build to Rent portfolio and a unique addition to Birmingham’s rental market – offering contemporary architectural design and amenities in a setting that maintains and reflects the Jewellery Quarter’s renowned heritage. We are excited to be working with our construction partners buildfifty5 and Pedrano UK on the project and look forward to seeing our vision for Great Hampton Street continue to come to life with new residents and independent businesses.”

András Kárpáti, CEO, Cordia UK

The Lampworks – located at the intersection of Great Hampton Street and Harford Street – will reflect the industrial heritage of Birmingham’s Jewellery Quarter. It forms part of Cordia UK’s wider vision for Great Hampton Street – a masterplan to transform the area into a thriving residential and commercial destination.

Specialist real estate investor and lender Octopus Real Estate (part of Octopus Investments) has provided financial support for The Lampworks, with assistance from financial advisor BBS Capital.

The loan was provided as part of its Greener Homes Alliance with Homes England, which pledges to commit £172m in finance and expert support to SME housebuilders, enabling them to build more high-quality, energy-efficient homes throughout England.

“We’re thrilled to have provided Cordia UK with the funding needed to develop this exciting project, conveniently located close to Central Birmingham. It’s a fantastic example of the impact our Greener Homes Alliance has in supporting developers to pursue greener initiatives, and reflects Octopus Real Estate’s commitment to providing quality, sustainable homes.”

Nick White, Head of Development Origination, Octopus Real Estate

As a member of one of the largest residential real estate development and investment groups in Europe, Cordia International (Member of Futureal Group), Cordia UK benefits from a vast track record of international projects and is driving forward innovative practices in the UK residential market.

Alternative lenders must navigate a market in which values are still unsettled and affordability is under pressure.

Interest rate rises have transformed real estate lending, causing the cost of debt to rise sharply, and delivering an unwelcome jolt to borrowers accustomed to the era of cheap credit. Lenders and sponsors in the mid-market now face a radically different business environment compared with 12 months ago.

The mid-market segment is not strictly defined, with market participants typically identifying it as €10 million to €20 million at the smaller end, defined by the point at which borrowers begin to access institutional capital market solutions, and €75 million to €100 million at its upper limit, the threshold at which big sovereign wealth, insurance company and private equity credit players begin to take more of an interest.

Many institutional real estate investment sales and development projects fall within that size bracket, but it is nonetheless a market that has historically been comparatively underserved by lenders, says Manja Stueck, managing partner, Europe debt, at manager BentallGreenOak.

“Underwriting a €20 million ticket is the same amount of work as a €100 million one. Not everyone has the team and the capacity to do it, and neither do they all want to do it. Now, with increasing interest rates and the other challenges we are seeing, it is even more work.”